Global aluminium markets are shifting again, with the US-Israeli war with Iran and broader instability across the Middle East adding a new layer of complexity to an already constrained aluminium supply environment. Emerging risks across key production and shipping corridors are accelerating upward pressure on the aluminium market.

Capral CEO Tony Dragicevich says these developments are reinforcing what the market has already been signaling. “We’ve been talking about a structurally tighter market for some time. What we’re seeing now is how quickly geopolitical events can amplify that pressure.”

Despite recent volatility, aluminium prices are expected to rise, with some analysts including Harbor Aluminum, forecasting it as high as $4,000 USD per tonne (Source:Harbor Aluminum, March 12 2026). This reflects increasing concern that instability in the Middle East could disrupt a region central to global aluminium supply.

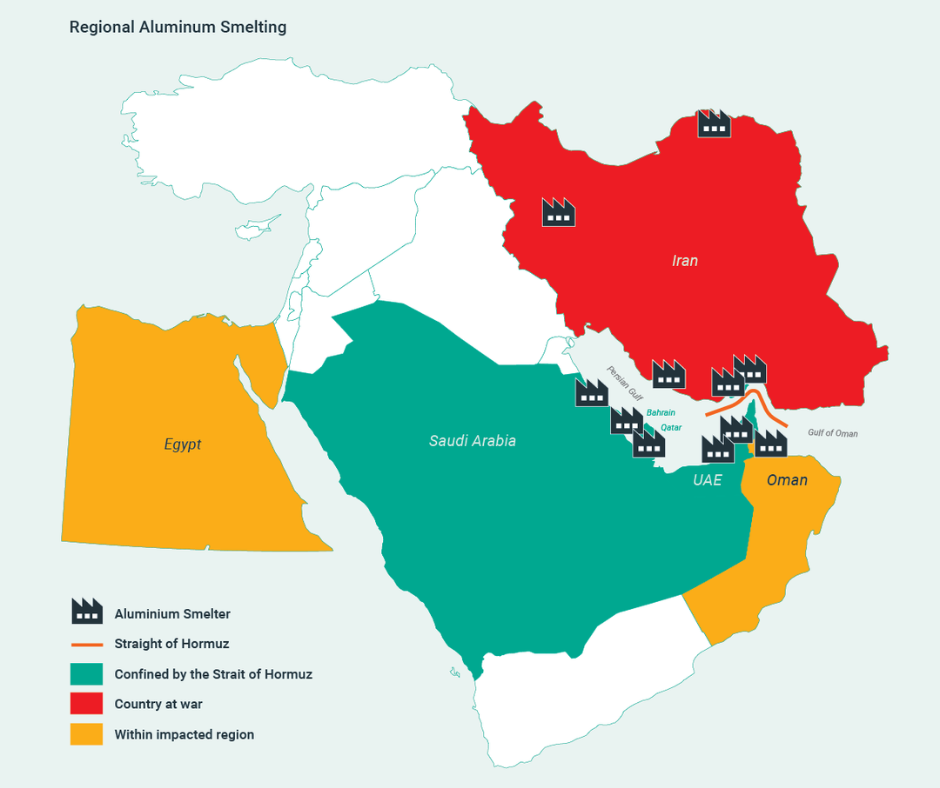

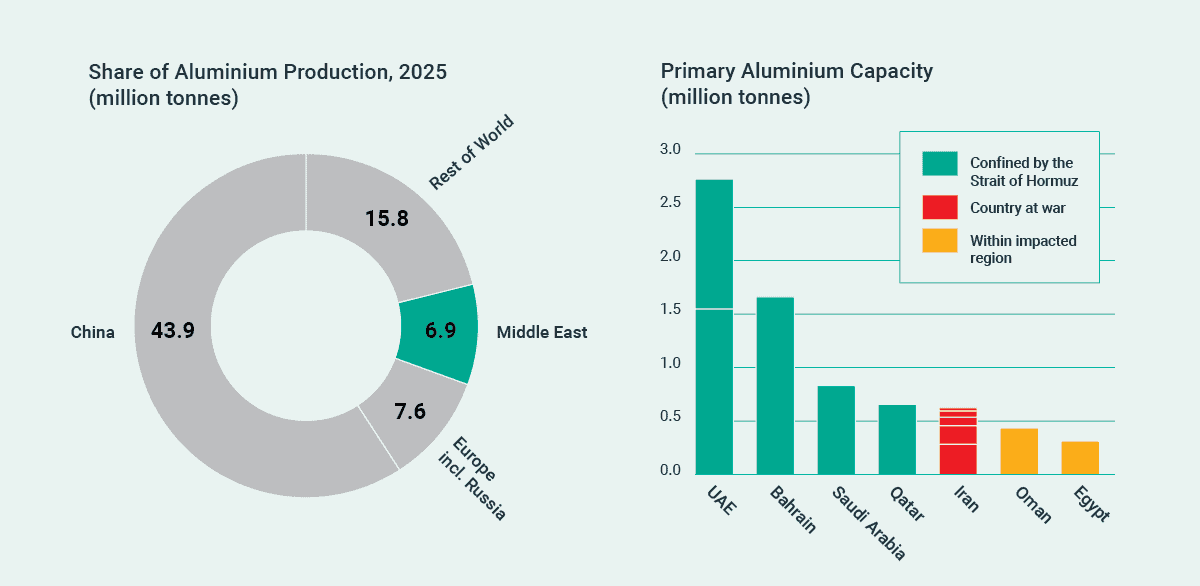

The Middle East accounts for roughly 9 per cent of global primary aluminium production. While this may appear modest, its importance is amplified by the region’s role as a key exporter to global markets. Any disruption, even temporary, can have an outsized impact on pricing.

At the centre of this risk is the Strait of Hormuz, one of the world’s most important shipping corridors. A significant portion of aluminium produced in the Gulf must pass through this narrow passage to reach international markets. When tensions rise and shipping through the strait is disrupted or restricted, the impact is immediate.

Delays, vessel rerouting and rising insurance costs all contribute to higher delivered prices. In some cases, material cannot move efficiently, tightening availability in key markets.

Recent developments have already demonstrated how quickly this can play out. Aluminium has reached multi-year highs in recent weeks as markets respond to the risk of disruption. Both Qatalum and Aluminium Bahrain (ALBA) have declared force majeure and implemented production curtailments, with Qatalum impacted by gas supply constraints and ALBA affected by disruptions to alumina supply. These developments are directly linked to the broader instability arising from the conflict within the region and are reinforcing concerns that supply could tighten further.

Tony notes that aluminium’s global nature makes it particularly sensitive to these types of events. “Aluminium doesn’t sit still. It moves to wherever it’s needed most, and it moves through global supply chains. When those chains are disrupted, the impact is felt everywhere, including here in Australia.”

The aluminium supply chain is highly interconnected. Smelters in the region rely on consistent energy supply and steady inbound flows of raw materials such as alumina, much of which is exported by Australia.

When shipping routes are constrained, the flow of alumina into the region can be disrupted, creating a cascading effect. Even if raw materials are available globally, delays in delivery can force smelters to reduce output or temporarily shut down.

Unlike many other industrial processes, aluminium smelting is not easily paused and restarted. Any interruption can remove supply from the market for an extended period, further tightening global availability.

This is why even the threat of disruption is enough to move markets.

The London Metal Exchange (LME) remains the global benchmark for aluminium pricing and responds quickly to shifts in supply risk. As uncertainty increases, prices adjust accordingly. In the current environment, where geopolitical tension is layered on top of already low inventories, expectations of constrained supply are pushing prices higher.

At the same time, regional premiums are rising. In the Asia-Pacific region, the benchmark premium is the Major Japanese Ports, or MJP. While the LME sets the global price, premiums reflect the cost of securing and delivering metal into specific markets. They act as an additional charge on top of the base LME price, capturing the real-world costs of freight, handling and logistics. Recent quarterly settlements have seen MJP premiums rise sharply, with deals reported around $350 USD per tonne, up from approximately $195 USD per tonne in Q1 2025. As shipping becomes more complex and supply chains lengthen, these premiums continue to increase, pushing up the final cost for manufacturers.

For Australian manufacturers, this reinforces the broader trend outlined in our previous update. Pricing pressure is not being driven by local demand conditions, but by global supply dynamics that continue to evolve.

Even where supply is secure, pricing is not insulated from these forces.

Capral continues to source the majority of its aluminium from domestic producers, providing a high level of supply reliability and continuity for its’ customers. However, aluminium remains a globally traded commodity, and pricing is fundamentally set by the London Metal Exchange.

Tony reinforces this point, saying, “We’re in a fortunate position in Australia with strong domestic supply, but we don’t operate in isolation. The LME sets the price, and that reflects what’s happening globally, not just locally.”

In addition to movements in LME and MJP pricing, Australian manufacturers are also facing increasing domestic cost pressures, particularly in fuel and transport. Diesel prices are experiencing significant volatility and sharp increases, with many locations exceeding $2.70 to $3.00 per litre as of 19 March 2026. Rising freight charges and ongoing pressure across the logistics sector are driving up the cost of moving aluminium within Australia.

“Given the size of the country and the reliance on road transport these costs are significant.”adds Tony.

For downstream manufacturers like Capral, this creates a layered cost environment. Global pricing sets the base, premiums add to the landed cost, and local freight further increases the price of supplying customers across the country.

Tony says the focus now is on transparency and partnership. “Our role is to keep our customers informed, stay reliable and help them during a challenging time. These pressures are real, but so is the resilience of Australian manufacturing.”

Looking ahead, the market will continue to be shaped by global forces, with supply holding but pricing remaining under pressure.